The flow to passive management is one of the biggest talking points of the decade. With this shift came the daunting task, and responsibility, to better evaluate the abundance of index funds offered by the marketplace. Index funds seek to replicate the performance of a benchmark, making the idea of comparing returns appear counter intuitive.

This notion has led many to focus almost entirely on fees. During this time period the industry experienced significant fee compression, with the difference between a few of the most commonly utilized index funds as small as 0.002%. This amounts to $2 for every $100,000 invested. Relative to the administrative burden to switch funds, investment cost is not the best method of selecting funds especially considering that shortly after, a different fund may be the new lowest-cost option.

How else can an index fund differentiate itself from its competitors – If not fees, what should be evaluated? The best index fund managers provide tight benchmark tracking at a reasonable price, and two techniques they can incorporate into their investment process are cross trading and securities lending.

Through the application of certain trading techniques, index managers can reduce cost and improve tracking. Over time the composition of indexes change, yet the process funds undergo to match these changes are complex. For example, as companies grow, they may move from the small cap index into the large cap index. For the index, this is a simple process. One day the company is in the small cap index and the next day they are in the large cap index. No trading needs to occur, no commissions paid, no bid-ask spreads crossed, no trades routed – yet funds must overcome these hurdles if they want to match the index’s performance.

One technique to overcome these challenges is through the use of cross trading. Suppose a fund company offers a small cap index fund and a large cap index fund and “company X” is being moved from the small cap index to the large cap index. The fund company could sell all their shares of “company X” in the small cap fund. This incurs cost and drives the price down as they sell. Then they buy all the shares back in their large cap fund, driving the price up as they buy. Through cross trading, this process is more streamlined. The fund company transfers their shares of “company X” from their small cap fund to their large cap fund without incurring costs. This leads to reduced tracking error and improved performance. To conduct due diligence on an index manager’s cross trading capabilities examine the index fund company’s cross trading process and review percentages of trades crossed.

The second method by which an index fund can be evaluated is through their use of securities lending. Securities lending refers to the temporary lending of a stock, derivative, or bond by one party to another in exchange for collateral. The collateral can be reinvested to produce income for the lender. Securities lending is important to short sellers who profit when securities drop in value. If an active investor is looking to short “stock ABC”, currently worth $100, they can borrow “stock ABC” from an index fund, offering the fund $103 as collateral. The index fund can invest this cash until the stock is returned, generating extra return, helping offset the costs the fund faces.

It is important to remember this is not risk-free money for the fund. This process exposes the fund to counterparty risk – which is when the active investor does not return the stock owed. The second is reinvestment risk – when the fund invests the $103 and it loses value. To mitigate this risk many fund companies have adopted SEC or OCC money market guidelines that outline the maturity, credit ratings, and liquidity restrictions on the collateral investment. Well established index providers will furnish information on their counterparty and collateral guidelines.

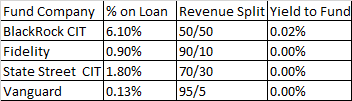

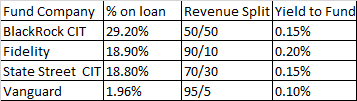

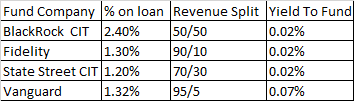

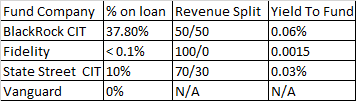

How much extra return can securities lending generate? Looking at the graphs below we can see significant additional return through securities lending, sometimes in excess of the management fee charged by the fund

500 Index Fund

Small Cap Index Fund

International Index Fund

Bond Index Fund

These complex features, prevalent amongst passive managers explain why RPAG tailored the scorecard to evaluate passive managers on analytics and metrics specific to, and important for, passive funds. On the surface it might seem counter intuitive to include an analytic on return rank for a passive fund designed to match the performance of a benchmark. However, by including return rank we evaluate a fund’s effectiveness in securities lending and cost reduction through cross trading.

Two analytics dedicated to tracking error may seem unnecessary, however performance matching is a primary objective of passive funds. It is critical for managers to utilize every tool in their toolbox. An emphasis on tracking error allows for better assessment of how well managers are meeting this objective. While fees are an important component of evaluating a passive manager, it is not the only data point, and the RPAG scorecard incorporates all significant components into the analysis.

For more information about cross trading and securities lending, reach out to SDMayer & Associates LLP.

About the Author

Ryan is an investment analyst for RPAG. He works closely with advisors and plan sponsors on manager due diligence and conducting market and fund research. Ryan is also a member of the RPAG Investment Committee, where all quantitative and qualitative aspects of the investment due diligence process are vetted and discussed when providing manager recommendations at the firm level for the firm’s entire client base. Ryan specializes in fixed income, cash vehicles, and alternative investments. Ryan graduated magna cum laude with a Bachelor of Arts from UCLA, and is a CFA Level III Candidate.

SECURITIES AND ADVISORY DISCLOSURE:

Securities offered through Valmark Securities, Inc. Member FINRA, SIPC. Fee based planning offered through SDM Advisors, LLC. Third party money management offered through Valmark Advisers, Inc a SEC registered investment advisor. 130 Springside Drive, Suite 300, Akron, Ohio 44333-2431. 1-800-765-5201. SDM Advisors, LLC is a separate entity from Valmark Securities Inc. and Valmark Advisers, Inc.

DISCLAIMER:

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. The services of an appropriate professional should be sought regarding your individual situation.

HYPOTHETICAL DISCLOSURE:

The examples given are hypothetical and for illustrative purposes only.